The Letwin review of build-out rates: A strong diagnosis but where next?

Daniel Bentley, 27 June 2018

Landbanking. Did ever a bit of jargon provoke such a range of passions as ‘landbanking’? The big developers’ annual reports are full of descriptions for investors about the size of their landbanks – so much as utter the word in their company though and they regard it as an affront to their dignity. Half the world is convinced that the developers are cynically landbanking to swell their profits – and yet review after review clears them of any such thing.

Landbanking. Did ever a bit of jargon provoke such a range of passions as ‘landbanking’? The big developers’ annual reports are full of descriptions for investors about the size of their landbanks – so much as utter the word in their company though and they regard it as an affront to their dignity. Half the world is convinced that the developers are cynically landbanking to swell their profits – and yet review after review clears them of any such thing.

The problem lies in the various meanings – some neutral, some pejorative – that are attributed to the same word. The interesting question is not so much whether developers have landbanks (they do), but what they are doing with them. A further – and potentially much more interesting – question concerns landbanking by individuals and firms other than developers; ie the non-builder interests who control the supply of land to the builders.

The Letwin Review, whose ‘draft analysis’ was published this week, investigates one aspect of this complex tangle of issues: the build-out rate of sites from the point at which they have a detailed and implementable planning permission to the point at which the final home is built. Sir Oliver Letwin was appointed amid growing interest in the significant gap between the number of new homes being approved by the planning system and the number of homes actually being built. This is not, then, a wide-ranging inquiry into the pipeline of land for development but a relatively narrow investigation into the final section of that pipeline – the point at which building is actually taking place. Considered as such, it is a useful analysis that brings some clarity to what is going on during the construction stage.

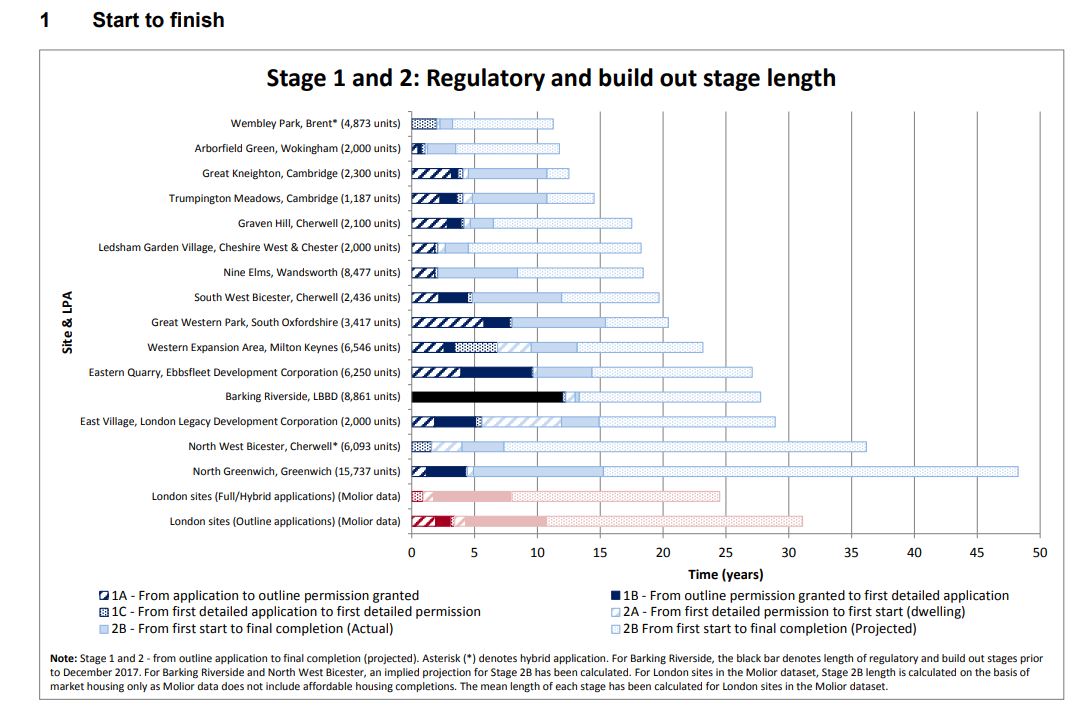

The headline findings will surprise nobody familiar with these issues: the median build-out period across the ‘very large’ sites that he studied was 15.5 years (the 44 years projected for one was eyebrow-raising though). The median proportion of a site built out each year was just 6.5 per cent. These numbers are based on quite a small sample of sites – just 15, ranging in size between 1,187 and 15,737 units – but they are broadly consistent with repeated studies and findings over the years. But what is interesting about the Letwin Review is, first, the conclusions it comes to about why these build-out rates are what they are and, second, where those conclusions are likely to lead in terms of proposals and potentially government reform.

There have been various efforts in recent years to explain away the build-out rate issue with reference to delays to development that arise prior to detailed planning consent. There are legitimate concerns in this area and Letwin’s case studies – detailed in the annex – describe many of the complexities that need to be dealt with from site to site. But these do not really have much bearing on what happens to a site once an implementable consent has been granted. This last is Letwin’s principal concern and – to his credit – he refuses to be distracted from it by other concerns. As is well known, and as the following chart from the review illustrates once more, the build-out period is usually a deal longer than the period spent securing planning consent.

This is not, he notes, due to lack of transport infrastructure, land remediation challenges or utilities delays – all require attention from government but none seriously affect build-out rates as they are usually dealt with before work starts. Nor is the build-out rate usually constrained by site logistics or materials and labour shortages. (He does raise a flag about the availability of sufficient bricklayers in future if housebuilding is to be stepped up, warning this would be a ‘biting constraint’ if build-out on large sites were to be increased very much.)

Another thing that does not cause slow build-out rates, he says, is the reluctance of developers to run down their land holdings too quickly due to the difficulty of getting planning permission for further supplies of land. This is a hobby horse of those with an ideological aversion to any kind of planning. Letwin rejects it, pointing out that probably more than 80 per cent of applications ultimately receive approval and, while the time taken to get that approval is ‘undoubtedly aggravating and sometimes costly’ for developers, it is ‘not actually so great as to cause problems of business continuity for major house builders with large property portfolios’:

‘…major house builders can expect to obtain new additions to their portfolios of land for development within three to four years – thereby enabling them to accelerate the rate of build out of current sites without any substantial fear of running down their stock of land supply to levels that would reduce their long-term sustainability.’

Finally, and the section that will have most cheered the housebuilders, is his conclusion that they are not holding land as a purely speculative activity and awaiting the moment of maximum profitability. Letwin does not extend the same vindication to landowners (of the non-building variety), however, noting:

‘I have heard anecdotes concerning land owners who seek to speculate in exactly this way by obtaining outline planning permission many years before allowing the land to have any real development on it – and I am inclined to believe that this is a serious issue for the planning system. But it is not one that is consistent with the business model of the major house builders.’

So, the developers aren’t ‘landbanking’ after all then? Well, not in this sense of the word. But in another sense, he says, ‘the major house builders are certainly “land banking”’. This is in the sense that, once they do start building, they do not do so at a rate that will materially affect the local market price. This is the market absorption rate, and when you strip away all of the excuses about planning delays and utilities and so on, this is what lies at the root of the slow build-out rates once developers get on site.

Again, this will not be news to many of those who have studied this issue, but it is helpful that Letwin has trained the spotlight on the primary difficulty, which starts with the fact that developers buy land at a value predicated on current prices in the second-hand housing market:

‘There is… a crucial assumption lying behind this method of valuation: namely, that the supply of new homes in the locality is not going to be sufficiently large to have any noticeably effect on the supply and demand balance in that local housing market, and is therefore not going to have any noticeable impact on the open market value of second-hand homes in that locality… In other words, the standard method of valuation for new housing used by all reputable valuers in the UK bakes in the assumption that local housing markets will not be ‘flooded’ with new homes to the point where current prices of second-hand homes in the local market are forced downwards.’

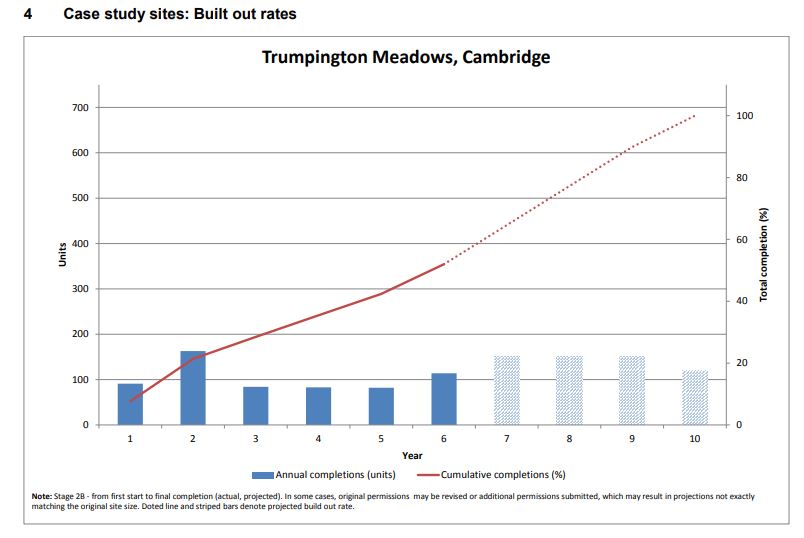

The absorption rate – what Letwin calls ‘the value-unaffecting rate of sale’ – determines the build-out rate and explains how you end up with a site of 1,187 homes taking a decade to build, as in this chart.

Builders simply cannot build faster than they call sell at the anticipated market price on which they valued the land. On Trumpington Meadows, the review notes that the cost of capital was ‘too great for building to slow down’ and yet ‘they had to wait for six months in mid-2016 for sales to catch up with rate of building’. At Nine Elms, the review was told that ‘developing all homes simultaneously would reduce sales prices’. At Arborfield Green, in Wokingham, ‘if site specific constraints such as land remediation were not an issue, they would not have built any faster’.

The expected absorption rate informs the entire construction process, from the phasing and financing to arrangements for the provision of labour, materials, remediation and infrastructure. Everything proceeds at a rate designed to ensure – reasonably – that the developer can recoup the cost of the land that they have bought at a price that assumes house prices do not fall (and indeed, Letwin notes, will further assume an ‘expected average rate of house price inflation across the anticipated period to completion’):

‘Once a house builder working on a large site has paid a price for the land that is based on the assumption that the sale value of the new homes will be close to the current value of second-hand homes in the locality, the house building company is not inclined to build more homes of a given type in any given year on that site than can be sold by the company at that value; and the house builder’s first customers (and indeed their mortgage lenders) may tend to be unenthusiastic if they see the prospect of homes of the same type on the same site being sold in such quantities as to reduce the prices obtained for those homes in the market after they have bought their own homes.’

What should be done about this will be the focus of a further update from Letwin at the time of the Autumn Budget. But his draft analysis provides some pointers. He does not want to do anything to disturb the assumptions on which developers currently price new-build homes: this would, he says, ‘create very serious problems not only for the major house builders but also, potentially, for the housing market and hence the economy as a whole’. So we can expect market housebuilding to be allowed to continue at its current ‘value-unaffecting rate’. He is not convinced, either, that relying on small sites holds the key. Larger sites are essential for the provision of infrastructure, while approving lots of small sites requires local authorities to ‘pick a multitude of small fights’ when it is ‘far easier to pick a few, larger fights’. He also suggests that breaking up larger sites into smaller sites would have the net effect of reducing build-out rates rather than increasing them.

Instead, the focus of Letwin’s thinking is on the scope for the diversification of output on individual sites. He argues that the absorption rate is especially limited due to the homogeneity of the homes that are being built – in mostly the same style and mostly for market sale. If there were a greater degree of ‘differentiation within sites’ – with housing of different types, designs and tenures, in more distinct settings, landscapes and streetscapes – then absorption rates and build-out rates could be ‘substantially accelerated’. This is undoubtedly true, and it is encouraging that Letwin is thinking along these lines. The big question over the coming months will be, how is this to be achieved – and indeed how ‘substantially’ can build-out rates be accelerated – within the model of development he has just outlined in his report?

As he notes, a prospective buyer who cannot afford a new-build home in the style offered may well be able to afford one in a different (cheaper) style. By the same token, greater variety in the architecture, interior design or landscaping may well tap additional sub-sections of the prospective market. But the current degree of uniformity, and the price range that developers are targeting, are not an accident that will be set right by the government simply pointing these things out – they are an outcome of the present market arrangements. Irrespective of the implications for build-out rates, what is at present produced by developers is what most efficiently delivers the returns they are seeking. It is part and parcel of a system in which developers bid up the price of land – necessarily, in order to secure it – to levels at which more imaginative design standards and architectural niceties are squeezed out.

Similar applies to the tenure mix. Letwin points – promisingly – to the ‘virtually unlimited’ demand for social housing as well build-to-rent, specialist housing for key workers and the retired, custom build and shared ownership. Again, though, the current tenure mixes are not as they are by mistake – they reflect the development opportunities that are on offer to the landowner at an earlier stage in the process; sub-market provision is already negotiated at – or close to – the limits of what the landowner is prepared to accept. Here Letwin’s interests start to overlap with the government consultation on developer contributions (such as Section 106 and the Community Infrastructure Levy), and the review of viability assessments that have such a bearing on how much affordable housing is provided alongside homes for market sale.

None of this is insurmountable and Letwin’s analysis has been useful so far in throwing the spotlight on what is really holding back build-out rates: the market absorption rate, accentuated by overly homogenous output. But in proposing solutions that make a substantial difference it may be necessary for him to delve a bit deeper into the forces that are determining and shaping that output. It might be necessary, even, to look a bit further back up the development land pipeline.

Daniel Bentley is editorial director at Civitas and the author of The Land Question: Fixing the dysfunction at the root of the housing crisis. He can be contacted at daniel.bentley@civitas.org.uk and tweets @danielbentley